Blockchain technology has gained significant attention and popularity in recent years, but its origins can be traced back to the 1990s. In this article, we’ll explore the history and evolution of blockchain technology, from its early beginnings to its current applications and potential for the future.

The origins of blockchain

In 1991, Stuart Haber and W. Scott Stornetta published a paper titled “How to Time-Stamp a Digital Document”, which outlined a method for creating a tamper-proof ledger by using cryptographic hashes. This early concept of a digital timestamping system laid the foundation for what would eventually become blockchain technology.

In 2008, an unknown person or group of people using the pseudonym “Satoshi Nakamoto” published a paper titled “Bitcoin: A Peer-to-Peer Electronic Cash System”. This paper introduced the concept of a decentralized digital currency that could be transferred without the need for a central authority.

The birth of Bitcoin

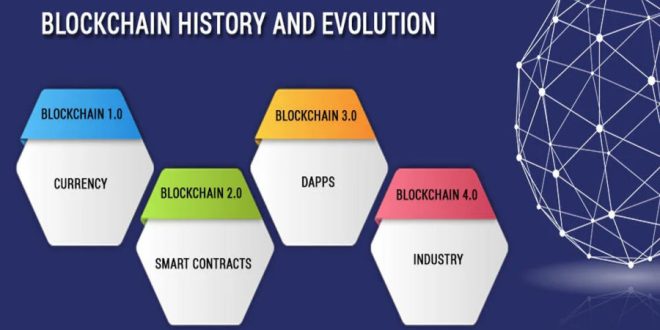

In January 2009, the first Bitcoin block, also known as the Genesis block, was mined by Nakamoto. This marked the beginning of the Bitcoin network and the first instance of a blockchain being used in practice. The Bitcoin blockchain is a public ledger that records all Bitcoin transactions and is maintained by a network of nodes, each of which stores a copy of the blockchain.

Bitcoin’s success and adoption

Bitcoin quickly gained popularity and became the dominant cryptocurrency in the market. It offered a decentralized and transparent system that could potentially disrupt traditional financial systems. The use of blockchain technology also opened up new possibilities for other industries beyond finance, including supply chain management, voting systems, and intellectual property rights.

As Bitcoin and other cryptocurrencies gained popularity, new blockchain networks were created, each with their own unique features and applications. These networks often use different consensus mechanisms and protocols, creating a diverse ecosystem of blockchain technologies.

The evolution of blockchain technology

While the early blockchain networks, such as Bitcoin and Ethereum, were focused primarily on financial applications, the potential for blockchain technology to be used in other industries quickly became apparent. In 2015, the Hyperledger project was launched by the Linux Foundation, with the goal of creating open-source blockchain software for use in various industries.

Since then, there have been significant advancements in blockchain technology, including the development of new consensus mechanisms, such as proof-of-stake, and the introduction of smart contracts. Smart contracts are self-executing contracts with the terms of the agreement between buyer and seller being directly written into lines of code. They are stored on the blockchain and are executed automatically when certain conditions are met. This has opened up new possibilities for automation and efficiency in various industries.

Another development in blockchain technology is the rise of enterprise blockchain solutions. Companies such as IBM and Microsoft have launched their own blockchain platforms, aimed at providing businesses with secure and scalable blockchain solutions.

Potential for the future

Blockchain technology has the potential to transform various industries, from finance to healthcare to supply chain management. Its decentralized and transparent nature offers increased security and trust, while its potential for automation and efficiency can lead to significant cost savings.

As the technology continues to evolve, it is likely that we will see new use cases and applications emerge. One potential area of growth is the use of blockchain technology for decentralized finance (DeFi) applications, which could offer a more accessible and transparent financial system for all.

The challenges and limitations of blockchain technology

While blockchain technology has shown great potential, it is not without its challenges and limitations. One major challenge is scalability, as the current blockchain networks are not capable of handling the same level of transactions per second as traditional centralized systems. This can lead to slower transaction times and higher fees, limiting the usability of blockchain technology for certain applications.

Another challenge is the issue of governance and regulation. The decentralized nature of blockchain technology can make it difficult to enforce regulations and standards, leading to concerns around illegal activity, such as money laundering and terrorist financing.

Additionally, there are concerns around the energy consumption of blockchain networks, particularly in the case of proof-of-work consensus mechanisms used by Bitcoin and other cryptocurrencies. This high energy consumption has led to criticism of blockchain technology’s environmental impact.

Finally, there are concerns around the potential for hacking and security breaches. While blockchain technology is inherently secure due to its use of cryptographic hashes and consensus mechanisms, there have been instances of exchanges and wallets being hacked, leading to the loss of millions of dollars worth of cryptocurrency.

Despite these challenges, the potential for blockchain technology to revolutionize various industries cannot be ignored. As the technology continues to evolve and new solutions are developed to address these challenges, it is likely that we will see wider adoption and integration of blockchain technology into our daily lives.

The future of blockchain technology

The future of blockchain technology is promising, with new developments and advancements being made every day. One potential area of growth is the use of blockchain technology for identity verification, allowing individuals to have greater control over their personal data and reducing the risk of identity theft.

Another potential area of growth is the use of blockchain technology for decentralized autonomous organizations (DAOs). These are organizations that are run entirely on the blockchain, with decision-making and operations being automated and decentralized. This could lead to a more democratic and decentralized form of governance for businesses and organizations.

The potential for blockchain technology to be used in the internet of things (IoT) is also significant. By integrating blockchain technology with IoT devices, it is possible to create a more secure and transparent network of devices, with greater control over data privacy and security.

Conclusion

In conclusion, the history and evolution of blockchain technology have been marked by significant advancements and innovation, as well as challenges and limitations. While there are concerns around scalability, governance, energy consumption, and security, the potential for blockchain technology to transform various industries cannot be ignored.

As the technology continues to evolve and new solutions are developed, it is likely that we will see wider adoption and integration of blockchain technology into our daily lives, leading to a more secure, transparent, and decentralized future.

I’m a professional writer specializing in cryptocurrency. I have over 5 years of experience writing about Bitcoin, Ethereum, Litecoin, and other digital assets. In addition to my work as an author, I’m also a highly respected speaker on the topic of cryptocurrency. I have spoken at numerous conferences and meetups around the world, and am always up-to-date on the latest developments in the space.